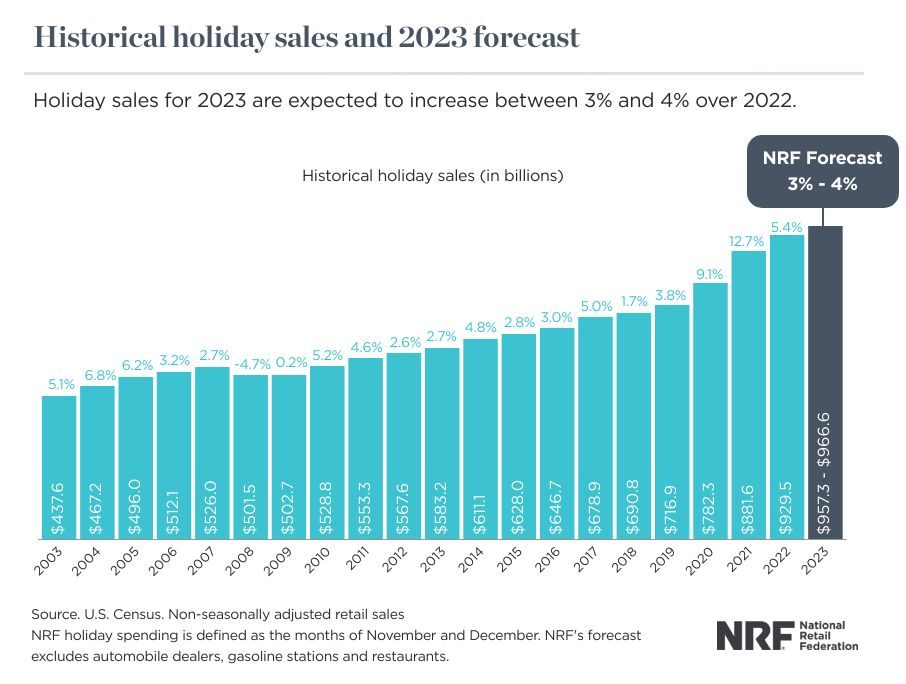

NRF forecast: holiday spending growth will return to pre-pandemic levels of 3% to 4% over 2022

Fastest growth areas for consumer spending are online shopping and the transition from goods to services

Holiday spending this winter is expected to reach record levels during November and December and will grow between 3% and 4% over 2022 levels to reach between $957.3 billion and $966.6 billion, according to a forecast released today from the National Retail Federation (NRF).

Despite a slower growth rate compared with the past three years, when trillions of dollars of stimulus led to unprecedented rates of retail spending during the pandemic, this year’s holiday spending is consistent with the average annual holiday increase of 3.6% from 2010 to 2019, NRF said.

“Consumers remain in the driver’s seat, and are resilient despite headwinds of inflation, higher gas prices, stringent credit conditions, and elevated interest rates,” NRF Chief Economist Jack Kleinhenz said in a release. “We expect spending to continue through the end of the year on a range of items and experiences, but at a slower pace. Solid job and wage growth will be contributing factors this holiday season, and consumers will be looking for deals and discounts to stretch their dollars.”

One of the chief areas where shoppers will be looking for deals is online. Online shopping has been one of the biggest shifts in consumer behavior from the COVID-19 pandemic. Online and other non-store sales, which are included in the total, are expected to increase between 7% and 9% to a total of between $273.7 billion and $278.8 billion. That figure is up from $255.8 billion last year.

Another area with fast spending growth is the service sector, NRF said. “For all that the consumer has kept the economy afloat, the composition of spending from goods to services will also define holiday sales trends,” Kleinhenz said. “Service spending growth is strong and is growing faster than goods spending. The amount of spending on services is back in line with pre-pandemic trends.”

A third area of change from past years is how soon shoppers will start hitting the stores. NRF’s latest holiday survey conducted by Prosper Insights & Analytics, which is separate from the holiday sales forecast, shows 43% of holiday shoppers planned to start making purchases before November.

That earlier start could have an effect on annual retail hiring trends. To meet the demand of the holiday season, NRF expects retailers will hire between 345,000 and 450,000 seasonal workers, in line with 391,000 seasonal hires in 2022. But some of this hiring may have been pulled into October to support retailers’ holiday buying events in October, NRF said.

NRF's holiday forecast is based on economic modeling that considers a variety of indicators including employment, wages, consumer confidence, disposable income, consumer credit, and previous retail sales. NRF’s calculation excludes automobile dealers, gasoline stations, and restaurants to focus on core retail. NRF defines the holiday season as November 1 through December 31.