Convergence is the word

If I had to describe the state of the third-party logistics (3PL) industry in one word, it would be convergence. Convergence refers to the merging of distinct technologies, industries, or devices into a unified whole. And that is exactly what is happening in this industry on two fronts.

The first involves the convergence of fragmented logistics services with integrated logistics solutions. This has been happening for many years, primarily via mergers and acquisitions. It is a path toward fulfilling the traditional definition (and promise) of a 3PL. Here is the Council of Supply Chain Management Professionals' definition:

A firm that provides multiple logistics services for use by customers. Preferably, these services are integrated, or "bundled" together by the provider. These firms facilitate the movement of parts and materials from suppliers to manufacturers, and finished products from manufacturers to distributors and retailers. Among the services they provide are transportation, warehousing, cross-docking, inventory management, packaging, and freight forwarding.

This convergence of services and broader solutions has also led logistics service providers to drive new growth by expanding globally to support clients across different geographic regions and by targeting new vertical industries, such as health care and energy. Here are just a few examples of this type of expansion from the first half of 2014, in the form of headlines from press releases:

- Transplace and Celtic Expand Intermodal Services in Mexico

- XPO Logistics Completes Acquisition of Pacer International

- Menlo Launches Freight Brokerage Service in Europe

- Coyote Logistics and Access America Transport to Merge

- UPS Continues Global Healthcare Expansion with Purchase of UK Healthcare Logistics Innovator

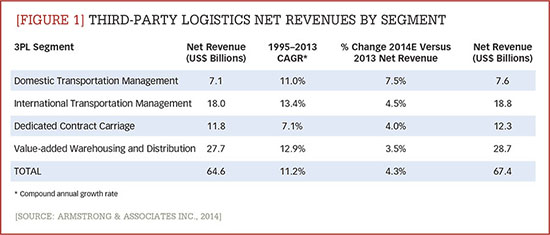

The trend toward the convergence of logistics services, coupled with the trend toward geographic and vertical industry expansion, will certainly continue in the months and years ahead as 3PLs fend off the risk of commoditization by positioning themselves as one-stop-shops or end-to-end solution providers. (Figure 1 shows the growth pattern for some of the major 3PL service segments.)

But there's another convergence taking place in the market, one that's driven by the changing needs and expectations of customers. This second convergence is transforming the very definition and value proposition of 3PLs. What we are seeing is the convergence of business models, specifically the business models of service providers, technology companies, and consulting firms.

There already are examples of logistics service providers offering their own software-as-a-service applications (C.H. Robinson and Transplace, to name two), and some consulting firms and software vendors are providing managed services (enVista, Transportation Insight, and LeanLogistics, for example). But that was just the beginning. In recent months, Amazon has embedded itself in Procter & Gamble (P&G) warehouses to fulfill online orders. Google has invested in its own fleet of vehicles to provide delivery services to consumers. And Uber has launched UberRUSH, a local delivery service that lets consumers use a mobile app to arrange for foot or bicycle messengers to pick up and deliver items weighing 30 pounds or less.

Simply put, the traditional definition of a third-party logistics provider is stale and limiting. It's becoming more outmoded every day as innovations in technology and business models continue to transform the competitive landscape. Logistics service providers that focus solely on the convergence of services and ignore the convergence of business models will, at best, limit their growth potential, and at worst, cease to exist.

WHAT BUSINESS ARE YOU IN?

What business are you in? That's a question every 3PL needs to ask itself today. As Anthony J. Tjan, chief executive officer and founder of the venture capital firm Cue Ball, wrote in a Harvard Business Review blog post titled "The First Strategic Question Every Business Must Ask," "It seems like a straightforward question, and one that should take no time to answer. But the truth is that most company leaders are too narrow in defining their competitive landscape or market space. They fail to see the potential for 'non-traditional' competitors, and therefore often misperceive their basic business definition and future market space."

That will likely sound familiar to many 3PL executives. But others are following the convergence path, not just providing customers with integrated logistics services like transportation management and warehousing, but also offering technology and business management services.

Some 3PLs, for example, provide software applications, trading partner connectivity, and data-quality management services that provide customers with timely, accurate, and complete visibility to supply chain events, information, and intelligence. Others provide thought leadership and advice, giving their customers new ideas that will help them make smarter and faster decisions about their supply chain networks, strategy, and practices. Some have risk management capabilities to help customers minimize or eliminate supply chain risks and, more importantly, to help them recover from supply chain disruptions more quickly and with less impact.

There are 3PLs that provide all of those things, yet most don't view themselves from those perspectives. But perhaps they should, because all of those services represent opportunities to differentiate themselves from the competition.

FOCUS ON OUTCOMES

What does this all mean for manufacturers and retailers looking for a logistics solution provider?

The first step remains the same: They have to clearly define their desired outcomes. But when it comes to finding the right partner to help them reach those objectives, they need to take a fresh look at the market—beyond the traditional labels of 3PL, software vendor, and consultant. The reality is that manufacturers and retailers have a diversity of options today, and regardless of how it may be labeled, the best outsourcing partner is the one that can provide the right mix of technology, services, and advice to help customers achieve their desired outcomes.

Manufacturers and retailers also have to recognize that the traditional way of managing 3PL relationships—viewing them as suppliers, with short-term agreements that are focused on providing the lowest-cost solution—is also becoming stale and limiting. To reach higher levels of performance and benefits, manufacturers and retailers need to start engaging in true collaboration and exploring vested relationships with their partners. ("Vested," a business model and methodology developed by the University of Tennessee, refers to outsourcing relationships that reward both partners for achieving mutually beneficial outcomes.)

And that would be the ultimate manifestation of convergence: 3PLs and customers developing a joint business plan and shared vision statement that align with the objectives and desired outcomes of the end customers, which in many cases are consumers like you and me.

Note: This story first appeared in the Special Issue 2014 edition of CSCMP's Supply Chain Quarterly, a journal of thought leadership for the supply chain management profession and a sister publication to AGiLE Business Media's DC Velocity. Readers can obtain a subscription by joining the Council of Supply Chain Management Professionals (whose membership dues include the Quarterly's subscription fee). Subscriptions are also available to nonmembers for $34.95 (digital) or $89 a year (print). For more information, visit www.SupplyChainQuarterly.com.