“State of Logistics Report” shows out-of-sync supply chains battling sharply rising costs

Volatility, inflation, and surging demand caused U.S. business logistics costs to increase by 22.4% in 2021.

Last year taxed every inch of the U.S. supply chain. At the same time that demand was surging, the industry was facing supply and labor shortages as well as tight capacity and a congested transportation network.

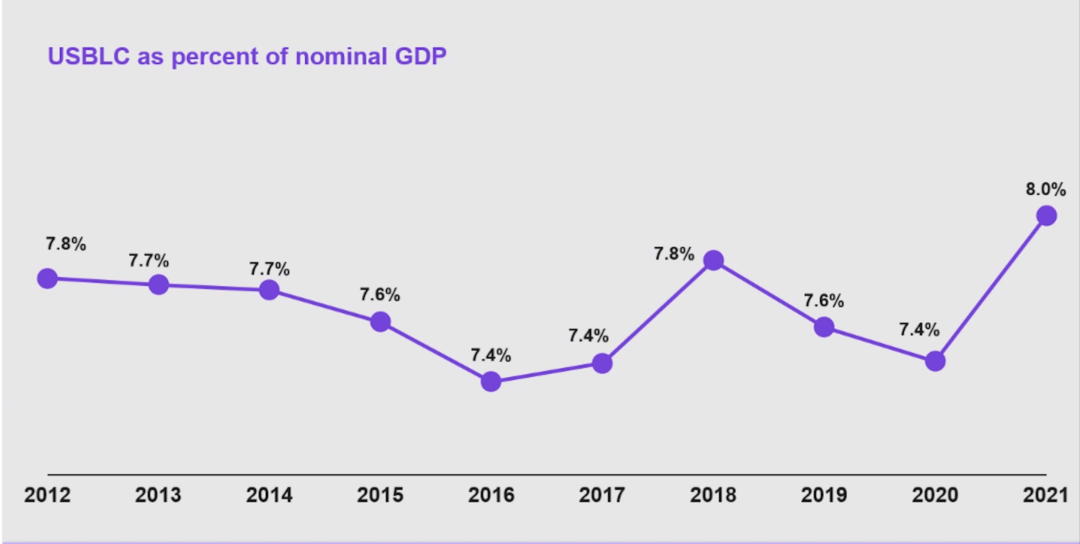

This volatility and tumult caused U.S. business logistics costs (USBLC) to skyrocket by 22.4% in 2021 to $1.85 trillion, according to the “33rd Annual Council of Supply Chain Management Professionals (CSCMP) State of Logistics Report.” As a result, USBLC ended up representing 8% of the country’s gross domestic product (GDP) of $23 trillion, a level not seen since 2008.

This year’s State of Logistics Report—a collaboration among the consultancy Kearney, the industry association CSCMP, and logistics service provider Penske Logistics—details all costs associated with moving freight through the U.S. supply chain. It also provides an analysis of the state of the economy and key logistics trends to watch. This year’s report describes a logistics system that was “out of sync” in 2021, with severe mismatches between demand and supply in everything from labor to transportation and warehousing capacity to supply for raw materials and supplies.

Due to these mismatches, inventory-carrying costs rose by 25.9% in 2021, and transportation costs increased by 21.7%. Furthermore, costs rose across the board in all modes and sectors, as can be seen in the breakdown below:

- Motor carriers: Trucking, which is the largest segment of U.S. logistics spend, saw its costs rise by 23.4% in 2021 to $831 billion. The increase was driven in part by rising consumer demand and shippers’ attempts to replenish inventory levels. Tight capacity drove many shippers to pay increasingly high spot market rates, which helped push profits for carriers upward. According to the report, top carriers reported seeing profits rise by 50% to 100%, and sometimes even more, even as their own operational costs surged.

- Parcel and last-mile logistics: E-commerce growth continued to benefit the parcel sector, which saw a five-year compound annual growth rate of 11.4%. Costs associated with parcel shipping rose to $134.5 billion, an increase of 15.2%.

- Rail: While network speeds and service levels dropped due to port congestion, chassis shortages, and a tight labor market, costs rose 18.8% to $88.3 billion.

- Air freight: With demand continuing to surpass supply, air freight costs also soared to $52.7 billion, an increase of 19.2%.

- Water shipping/ports: U.S. water shipment costs (which do not include international ocean expenditures) saw the biggest increase, shooting up by 23.6% to $32.4 billion. According to the report, ocean carriers earned more in 2021 than in the previous 20 years combined.

- Warehousing: Demand for warehousing space increased last year, while costs rose. Vacancy rates dropped to 3.7%, while rents rose by 9.5%.

While there is certainly the sense that last year’s challenges were unique and caused in part by the continuing COVID-19 pandemic, the logistics industry has been seeing significant volatility for a while. In 2018, logisticians were reeling from an 11.4% increase in logistics cost. While costs stabilized in 2019—growing just 0.6%—they dropped by 4% in 2020, the year of the pandemic shutdowns.

“It’s not surprising that we are continuing to see ongoing disruptions related to the pandemic,” Balika Sonthalia, partner at Kearney and lead author of the report, said, “but the scope and impact of disruptions continue to weigh heavily on the minds of logistics providers—as they do for all companies contributing to the U.S. economy.”

These disruptions indicate a greater need to focus on supply chain resiliency and agility and have encouraged companies to reassess their supply chain strategies and experiment with different approaches, both large and small. Many companies, for example, are increasingly turning to private and dedicated fleets for over-the-road shipping, while others have increased their use of air freight or are holding more inventory on hand. Other trends include an increase in merger & acquisition activity among transportation providers; greater interest in “multi-shoring” (or sourcing from more than one geographical location); and more investment in technologies, such as control towers, that improve supply chain visibility.

Looking forward, Sonthalia anticipates that 2022 will see a softening in demand for logistics services, particularly as many companies have seen their inventory-to-sales ratios increase this year. Capacity, however, will continue to remain tight, as the semiconductor shortage, high steel prices, and continuing labor market tightness will continue to make it difficult to deploy more equipment or capacity.