All hail the e-commerce consumer

Rapid growth in e-commerce is placing big demands on fulfillment networks. That pressure has been a constant for years, but the fallout is ongoing, as retailers and third-party logistics service providers (3PLs) scramble to find ever-faster and more efficient ways to fill small multiline-item orders.

The pressure shows no sign of abating; just witness e-commerce megalith Amazon.com Inc.'s announcement in April that it would ratchet up its Amazon Prime subscription-shipping plan from standard two-day delivery to one-day delivery. The announcement sent ripples throughout the industry, with retailers and carriers alike predicting the change will lead consumers to demand even faster fulfillment.

"The development of raised customer expectations for 'one-day' business-to-consumer (B2C) delivery capabilities could create additional headwinds to parcel providers' [profit] margins," Benjamin Hartford, a transportation analyst for investment firm Robert W. Baird & Co. Inc., said in a note to investors. "Amazon's creation of customer demand and expectations for B2C led to e-commerce's rapid development over the past 10 to 15 years. As a result, we recognize the risk of a similar headwind being presented to parcel providers if the migration to free 'one-day' becomes adopted and expected in customer preferences."

"The development of raised customer expectations for 'one-day' business-to-consumer (B2C) delivery capabilities could create additional headwinds to parcel providers' [profit] margins," Benjamin Hartford, a transportation analyst for investment firm Robert W. Baird & Co. Inc., said in a note to investors. "Amazon's creation of customer demand and expectations for B2C led to e-commerce's rapid development over the past 10 to 15 years. As a result, we recognize the risk of a similar headwind being presented to parcel providers if the migration to free 'one-day' becomes adopted and expected in customer preferences."

So where will the industry go from here? To get a better understanding of emerging fulfillment trends, DC Velocity teamed up with ARC Advisory Group, a Dedham, Mass., management consulting firm, to examine warehousing and fulfillment practices in the age of online shopping. Together, we conducted a broad industry study that looks at how practitioners are currently meeting the demands of e-commerce as well as their plans for the future.

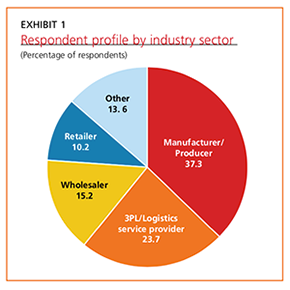

The study was conducted among 59 logistics professionals from a variety of industry sectors (see Exhibit 1) and is a sequel to a 2016 research project, allowing us to measure the trajectory of change in warehouse operational profiles, market pressures and priorities, warehouse order-fulfillment profiles, and warehouse technology. What follows is a look at some of the key findings.

MORE CHANGES AHEAD?

Industry trends aside, what ultimately determines how a given DC operates—from its processes and priorities to its equipment and technology—is the type of fulfillment it's engaged in: traditional store replenishment, DC replenishment, drop shipping, or direct-to-consumer shipping. A facility that mainly handles bulk orders for store replenishment will look quite different from one that primarily plays in the e-commerce arena.

To learn more about the study participants' operations, the researchers asked them which types of fulfillment their facilities supported. DC replenishment topped the list in this year's study, followed in rank order by direct-to-consumer/e-commerce fulfillment, direct fulfillment of a retail partner's customers' orders (drop shipping), and traditional store replenishment.

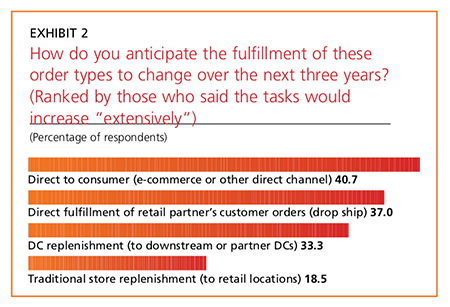

However, it appears the situation is in flux. When the study participants were asked how they expect those fulfillment activities to change over the next three years, their responses indicated that a big shift is under way. Some 40 percent said they expected direct-to-consumer fulfillment to increase "extensively," and a similar proportion said they expected a significant rise in drop shipping. A significantly smaller number said they expected to see an increase in replenishment shipments to partner DCs or retail stores. (See Exhibit 2.)

What the study makes clear is that DCs fully expect to continue focusing on e-commerce direct-to-consumer orders and drop-ship work, where they essentially serve as the fulfillment arm of their downstream partners such as e-tail websites, said Clint Reiser, director for supply chain research at ARC Advisory Group. Reiser, who led the study, noted that even as the volume of e-commerce orders continues to rise, warehouse shipments for store fulfillment are staying flat or declining, as traditional retailers reduce store footprints and trim inventory.

In a parallel finding, participants also indicated that they expected the type of picking performed at their facilities to shift over the next three years. When asked what changes they foresaw to their picking patterns, nearly half (48 percent) said they anticipated an extensive increase in piece picking. By way of comparison, just 26 percent said they expected a big jump in pallet picking and 19 percent in carton/case picking.

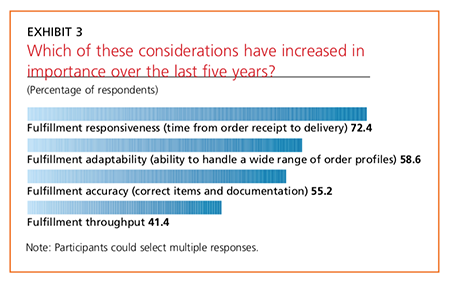

In order to navigate this shifting landscape, many companies have realigned their fulfillment priorities over past five years. Not surprisingly in an era when shoppers have come to expect instant gratification, speed has become a top priority for most operations. Our study participants are no exception. Asked which capability has grown most in importance over the past five years, 72 percent of respondents said "fulfillment responsiveness" (the time from order receipt to delivery). Lagging well behind were "fulfillment adaptability" (the ability to handle a wide range of order profiles), "fulfillment accuracy" (correct items and documentation), and "fulfillment throughput." (See Exhibit 3.) The rising importance of responsiveness shows that DCs are placing increased emphasis on prompt fulfillment in response to shifting consumer expectations for same-day or next-day delivery, Reiser said.

In order to navigate this shifting landscape, many companies have realigned their fulfillment priorities over past five years. Not surprisingly in an era when shoppers have come to expect instant gratification, speed has become a top priority for most operations. Our study participants are no exception. Asked which capability has grown most in importance over the past five years, 72 percent of respondents said "fulfillment responsiveness" (the time from order receipt to delivery). Lagging well behind were "fulfillment adaptability" (the ability to handle a wide range of order profiles), "fulfillment accuracy" (correct items and documentation), and "fulfillment throughput." (See Exhibit 3.) The rising importance of responsiveness shows that DCs are placing increased emphasis on prompt fulfillment in response to shifting consumer expectations for same-day or next-day delivery, Reiser said.

THE RUSH TO AUTOMATE

In order to reach those goals, DCs are investing in warehouse technologies such as software and automated equipment. In this regard, they have plenty of options. Visit any logistics trade show, and you'll find a wide array of products and services promising to supercharge fulfillment operations, from autonomous mobile robots (AMRs) to radio-frequency identification (RFID) tags.

In order to reach those goals, DCs are investing in warehouse technologies such as software and automated equipment. In this regard, they have plenty of options. Visit any logistics trade show, and you'll find a wide array of products and services promising to supercharge fulfillment operations, from autonomous mobile robots (AMRs) to radio-frequency identification (RFID) tags.

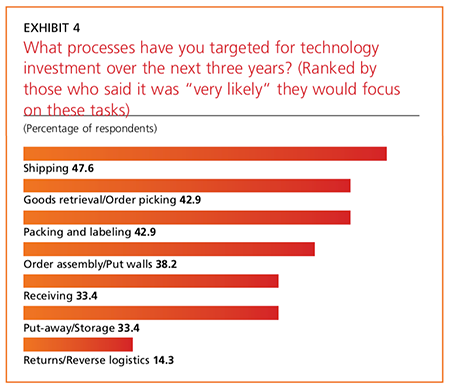

But no single technology can solve every challenge, so our study asked exactly what "material flow processes" companies were targeting for improvement through technology investments. The top three responses were shipping, goods retrieval and order picking, and packing and labeling. (For the full rundown, see Exhibit 4.)

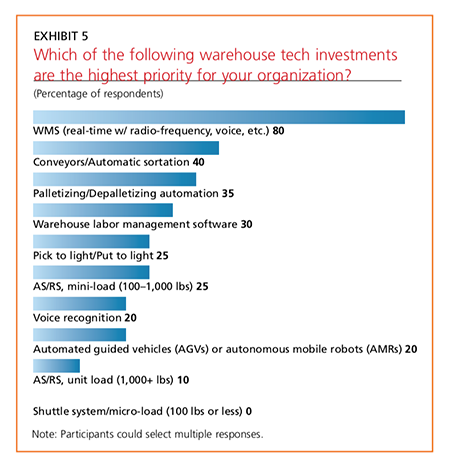

Next, we drilled down to ask exactly which warehouse tools were their top priorities for investment over the next three years. Here, the number-one vote getter was warehouse management system (WMS) software, followed by conveyors/automatic sortation, automated palletizing/depalletizing equipment, warehouse labor management software, and pick-to-light/put-to-light systems. (See Exhibit 5.)

Next, we drilled down to ask exactly which warehouse tools were their top priorities for investment over the next three years. Here, the number-one vote getter was warehouse management system (WMS) software, followed by conveyors/automatic sortation, automated palletizing/depalletizing equipment, warehouse labor management software, and pick-to-light/put-to-light systems. (See Exhibit 5.)

All of these choices align with shippers' need to accelerate delivery speed and wring the maximum efficiency out of their resources, Reiser observed. "WMS still reigns supreme as a must-have in a fulfillment operation, and labor management remains critical for obtaining efficiencies out of your operations," he noted. "Conveyor and sortation remains surprisingly important," Reiser added. "Even though other automation technologies are higher profile or 'sexier,' conveyance and sortation is still ubiquitous in warehousing."

E-COMMERCE STILL DRIVING THE TRAIN

These changes in warehouse picking patterns and processes underline the continuing impact of the e-commerce trends we first identified in the 2016 study on warehouse operations. Just as they are today, facilities back then were seeing a widescale shift away from the traditional pallet- and case-picking operations toward piece picking.

Participants in both studies also sent a consistent message when it came to the process "pain points" they most wanted to address with new technologies. The top two responses from the 2016 study—shipping and goods retrieval/order picking—remained unchanged in the 2019 study.

Then as now, consumer expectations are driving sweeping change in warehouses across the country as operations scramble to rev up fulfillment. As shoppers' expectations continue to ramp up, look for further changes in the warehousing universe as DC leaders rethink their processes, technology requirements, operational priorities, and even their role in the supply chain.